2026 U.S. Home Appliance Market: Tailwinds and Growth Opportunities

May 25,2026

111

In 2026, the U.S. economy is staging a moderate recovery driven by easing inflation, stable employment, and rebounding consumer confidence, creating an exceptionally favorable market environment for health-focused small kitchen appliances (SKAs) such as blenders, food processors, and juicers. The confluence of multiple positive drivers—including a recovering macroeconomy, rising health consumption trends, technological iterations, optimized channel structures, and policy dividends—has propelled the U.S. small appliance market into a golden growth period marked by simultaneous growth in both sales volume and average selling price (ASP). Among these, blenders, as the core equipment for healthy kitchens, have emerged as one of the fastest-growing categories with the strongest premium capability.

1. Stabilizing Macroeconomic Recovery Unlocks Consumption Potential for Small Appliances

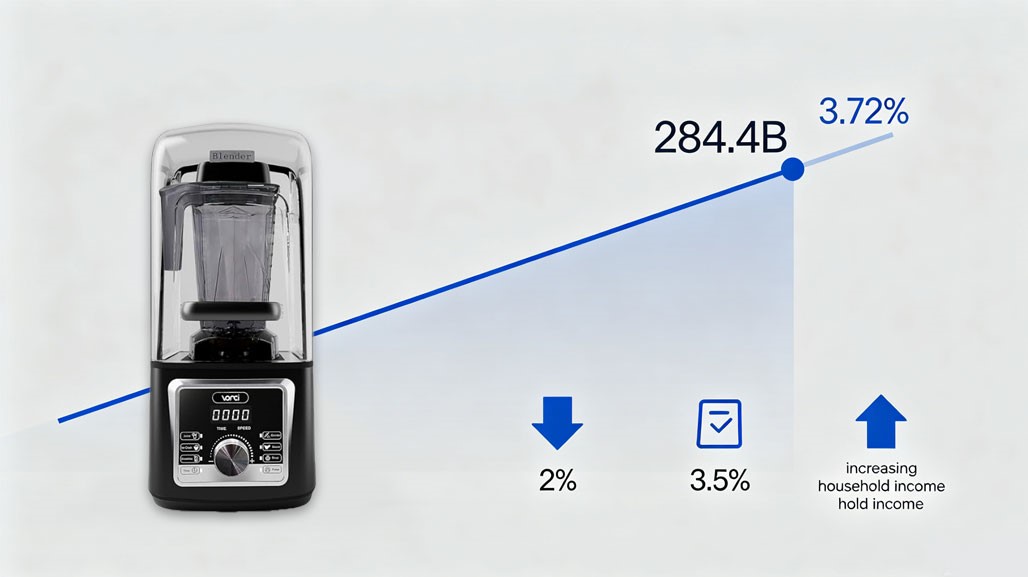

In early May, following China-U.S. economic talks, the economy demonstrated a positive trajectory of moderate growth, moderating inflation, and resilient employment, laying a solid economic foundation for small appliance consumption. According to the latest report from NIQ GfK, the U.S. small appliance market is projected to reach $28.44 billion in 2026, representing a year-over-year increase of 3.72%. The blender segment, in particular, is seeing outstanding growth, with sales expected to exceed $1 billion, and a compound annual growth rate (CAGR) staying above 6%. Easing inflationary pressure stands as the core positive driver. The U.S. inflation rate gradually fell below 3% in 2025 and is further stabilizing at around 2% in 2026, driving a steady recovery in residents' real disposable income. For small appliances like blenders priced between $100 and $500, moderating inflation has lowered the consumption threshold, allowing households that postponed replacement purchases due to elevated prices to release pent-up replacement demand in a concentrated manner in 2026. Meanwhile, the start of the Federal Reserve's rate-cut cycle has driven down loan rates, which not only reduces residents' consumer credit costs but also eases production and inventory pressure for enterprises, making end-product prices more competitive to further stimulate market demand.

The stable job market underpins consumer confidence. The U.S. unemployment rate is holding at a low level of around 3.5% in 2026, with nonfarm payrolls continuing to grow. In particular, the expansion of high-paying positions has led to a steady expansion of the middle-class population. As the main consumer group for small appliances, the middle class's purchasing power and willingness directly determine the market size. Data shows that the annual small appliance spending of U.S. middle-class households has increased by 18% compared with five years ago, with the share of spending on health-focused small appliances rising to 35%, making products such as blenders and air fryers standard kitchen fixtures for households. In addition, the moderate recovery of the real estate market has driven incremental demand. U.S. home transaction volume increased by 5% year-over-year in 2026, with active transactions in both new and existing homes. New home renovations and existing home upgrades have directly boosted purchases of kitchen small appliances; on average, each new home is equipped with 1.2 blenders and 0.8 food processors. The real estate recovery has injected incremental space into the market, forming a positive cycle of "economic recovery—real estate activity—small appliance sales boom".

2. Deepening Health Consumption Trends Elevate Blenders to a Core Necessity Category

Health-oriented, convenient dietary trends continue to deepen in the U.S. market in 2026, serving as the core driver of surging demand for health-focused small appliances like blenders. In the post-pandemic era, U.S. consumers have significantly raised their health awareness, with over 70% of consumers listing "healthy eating" as their top life priority, and plant-based diets, homemade nutritious meals, and additive-free beverages have become mainstream lifestyles. With its features of multi-functionality, nutrient extraction, and convenience, blenders perfectly align with these demands, evolving from an optional small appliance to a necessary kitchen fixture. According to data from the U.S. Department of Agriculture (USDA), nearly 70% of North American consumers regularly consume fruit and vegetable juices, plant-based milk, or protein shakes in 2026. As the core production tool, blenders have reached a household penetration rate of 71%, with an annual growth rate of 3% to 5%. Compared with traditional juicers, blenders can release full food nutrition by grinding hard ingredients such as nuts, seeds, and grains, meeting consumers' demand for high-nutrient-density diets, especially addressing the dietary needs of fitness enthusiasts, vegetarians, families with infants, and middle-aged and elderly groups.

Meanwhile, the trend of "homemade meals replacing takeout" has continued to solidify. U.S. takeout prices have risen by 25% compared with pre-pandemic levels in 2026, coupled with frequent food safety concerns, driving more consumers to turn to home cooking. Blenders can quickly prepare breakfast smoothies, lunch soups, dinner sauces, and baby food, significantly reducing meal preparation time to adapt to the fast-paced U.S. lifestyle. Data shows that households with blenders have increased their frequency of homemade meals by 40% and reduced takeout spending by 30%, and this dual advantage of cost-effectiveness and healthiness continues to drive blender demand growth. In addition, demand from specialized commercial scenarios has expanded the market space: commercial venues such as cafes, juice bars, light food restaurants, and wellness studios have strong demand for high-performance blenders, contributing 38% of market sales. Meanwhile, medical institutions and elderly care facilities use blenders for liquid food preparation, further broadening application scenarios to form a dual-driven growth pattern of household and commercial demand.

3. Technological Iteration and Premiumization Drive Volume-Price Growth for the Market

The U.S. blender market in 2026 is showing a clear trend of premiumization, intelligence, and multi-functionality. Technological iteration has not only enhanced product competitiveness but also driven a steady rise in average selling price, achieving the dual positive of volume growth and price increase. The premiumization trend is remarkable, with premium capability continuing to improve. The market is divided into three tiers: mass-market (under $100), mid-range ($100-$300), and premium (above $300). In 2026, the sales share of premium models increased from 25% in 2025 to 35%, with the average selling price exceeding $400. Consumers are willing to pay a premium for high-performance, durable brands; local premium brands such as Vitamix and Blendtec occupy 60% of the premium market, becoming the first choice for quality-conscious consumers thanks to their over 10-year service life, powerful motors, and full-ingredient processing capabilities. Meanwhile, mid-range products are seizing market share through functional upgrades, with their average price rising by 12% year-over-year, driving up the overall market average price and expanding industry profit margins.

Intelligent technology is accelerating penetration to reshape product value. The penetration rate of smart blenders exceeded 45% in 2026, becoming the industry's core selling point. Smart models are equipped with functions such as APP control, voice assistant linkage, preset programs, nutrition monitoring, and self-cleaning, supporting remote mobile operation and hundreds of built-in recipes to adapt to different ingredients and dietary needs. Their smart interconnection function can also access smart home ecosystems such as Amazon Alexa and Google Home for voice control, aligning with the U.S. smart home popularization trend. Data shows that smart blenders have an average price 30% to 50% higher than ordinary models, but their sales growth rate is twice as fast, making them the core engine of market growth. In addition, multi-functional integration has become the mainstream: blenders have evolved from single-function juicers to an all-in-one cooking center, integrating grinding, meat mincing, dough kneading, heating, and steaming to replace multiple small appliances. This design saves kitchen space for small U.S. homes and reduces consumption costs, winning favor among young urban groups. Technological upgrades such as silent technology, variable frequency motors, and energy-saving designs have further improved user experience, with sales of silent blenders rising 55% year-over-year and energy-saving model penetration reaching 60%.

4. Optimized Channel Structure and Stable Supply Chain Empower Efficient Market Expansion

In 2026, the U.S. small appliance channel structure continues to optimize, with integrated online and offline development. Coupled with the gradual stabilization of the global supply chain, this has effectively reduced circulation costs, improved product accessibility, and provided strong support for market growth. The leading position of online channels has been consolidated, while the Direct-to-Consumer (DTC, a business model that sells products directly to consumers without intermediate distributors) model is rising rapidly. Online sales account for 60% of total small appliance sales, and this figure exceeds 70% for blenders, with platforms such as Amazon, Walmart.com, and Target.com as the main sales channels. DTC brands reach consumers directly through independent official websites, social e-commerce, and live streaming, reducing intermediate links to increase profit margins. In 2026, blender sales through the DTC channel increased by 25% year-over-year, as young brands build product awareness through social platforms such as TikTok and Instagram to quickly seize market share. Online channels' transparent pricing, rich categories, and convenient delivery adapt to U.S. consumers' online shopping habits, especially promoting the popularization of mid-to-low-end products.

Offline channels focus on experiential marketing to drive premium scenario-based sales. Large supermarkets such as Walmart, Target, and Bed Bath & Beyond, as well as professional home appliance chains, have set up blender experience zones to demonstrate functions and offer tasting samples, enhancing consumers' purchase intention. Premium brands lay out boutiques and department store counters to focus on quality service for high-net-worth consumers. Offline channels also undertake after-sales maintenance and installation services to complement online channels, forming a complementary online-offline pattern. Meanwhile, the stabilized supply chain has reduced costs and ensured supply: ocean freight and raw material prices have fallen, and core blender components such as motors, glass jars, and blades are in sufficient supply. U.S. brands have deepened cooperation with manufacturing bases in China, Mexico and other regions to boost production capacity, alleviating previous stockout and price hike issues. Tariff optimization has also cut import tariffs for some small appliances, further reducing costs to make end products more competitive.

5. Policy Dividends and Sustainability Trends Empower Long-Term Growth

The U.S. policy orientation and sustainable development trends in 2026 provide long-term growth momentum for the small appliance market, driving the industry's upgrade toward energy efficiency and environmental protection. Energy efficiency policies are driving product upgrading, with strong green demand. The U.S. Department of Energy (DOE) will implement new kitchen appliance energy efficiency standards in 2028, and the preheating effect in 2026 has driven enterprises to increase investment in energy-saving technology R&D. As a high-power small appliance, blenders are seeing rapid growth in demand for energy-saving models; products with variable frequency motors and low-power design not only enjoy policy subsidies but also meet consumers' energy-saving needs. Data shows that sales of energy-saving blenders increased by 40% year-over-year in 2026. Although their average price is 15% higher than ordinary models, they can save 30% on electricity bills during long-term use, delivering significant cost-effectiveness.

Sustainable consumption trends are emerging, with environmentally friendly products increasingly favored. Over 60% of U.S. consumers now prioritize small appliances made with recyclable materials, eco-friendly packaging, and low energy consumption. Blender enterprises are responding by adopting food-grade stainless steel, recyclable plastics, and eco-friendly sealing strips to reduce harmful substances, while optimizing packaging to cut plastic waste. This sustainable concept not only enhances brand image but also aligns with U.S. environmental policies, forming a positive cycle of policy guidance, enterprise transformation, and consumer recognition. In addition, tax incentives and consumption subsidies are stimulating demand: the U.S. government extended the energy-efficient home appliance tax credit policy in 2026, allowing consumers to enjoy a 10% to 15% tax deduction for qualifying blenders. Some state governments have also launched green consumption subsidies to further lower costs and stimulate mid-to-low-end market demand, promoting the popularization of energy-saving blenders and supporting long-term healthy market development.

Against the backdrop of multiple positive factors including macroeconomic recovery and policy dividend release, VONCI blenders, as core kitchen equipment, have become the core engine of market growth thanks to their necessity attribute, premiumization potential, and diverse application scenarios. The blender segment is expected to maintain a compound annual growth rate of over 6% in the next five years. According to market research, a number of small appliance enterprises including VONCI are expected to embrace further growth space.